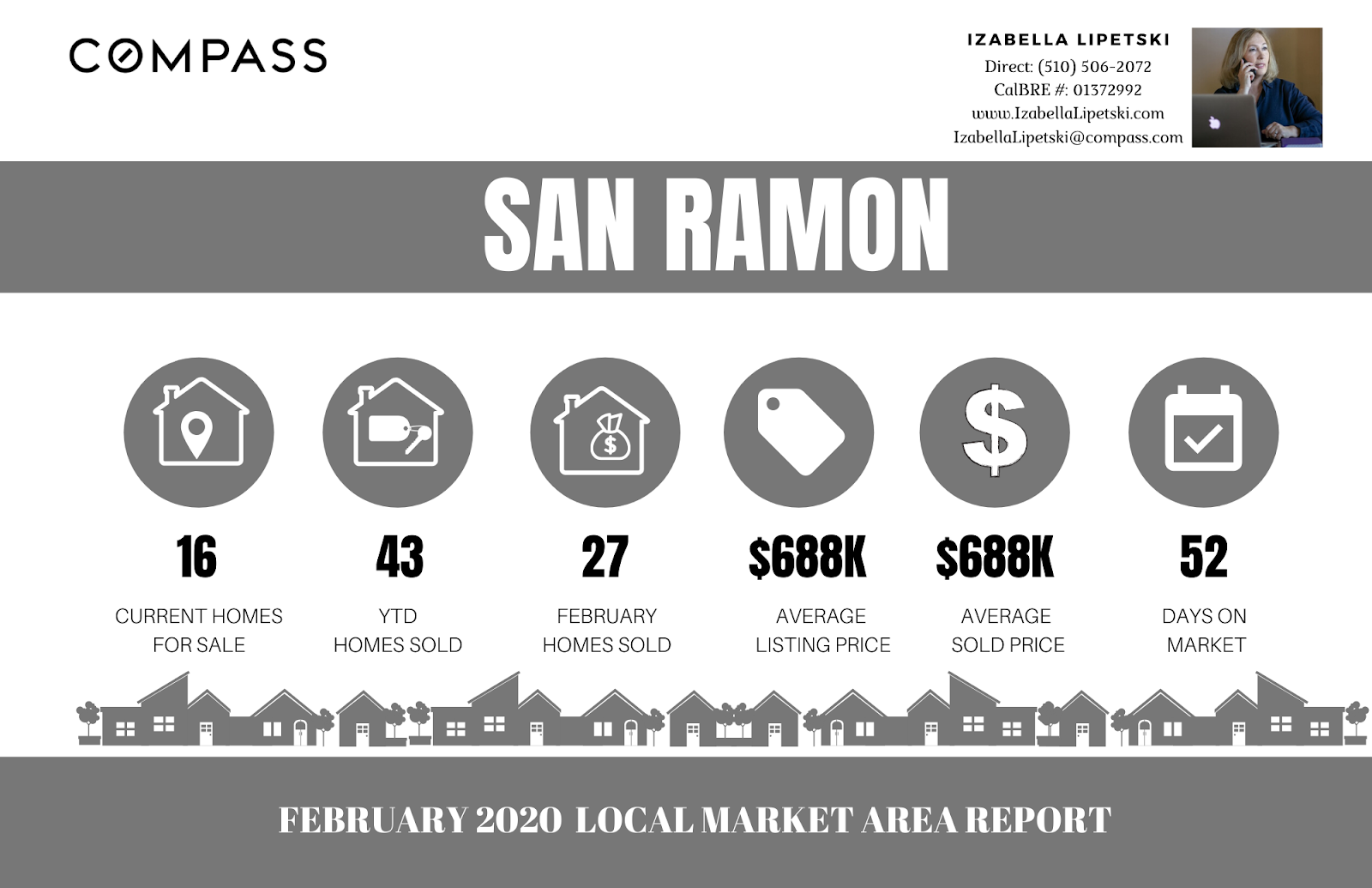

🏡 Buying or Selling Your Home? It's always a good idea to know what's going on in the market. 📊📈📉

Here's how the Real Estate Market performed FOR JULY 2020 for Pleasanton, Danville, Alameda, Oakland and San Ramon.

SINGLE DETACHED HOMES

🏡 Buying or Selling Your Home? It's always a good idea to know what's going on in the market. 📊📈📉

Here's how the Real Estate Market performed FOR JULY 2020 for Pleasanton, Danville, Alameda, Oakland and San Ramon.

SINGLE DETACHED HOMES

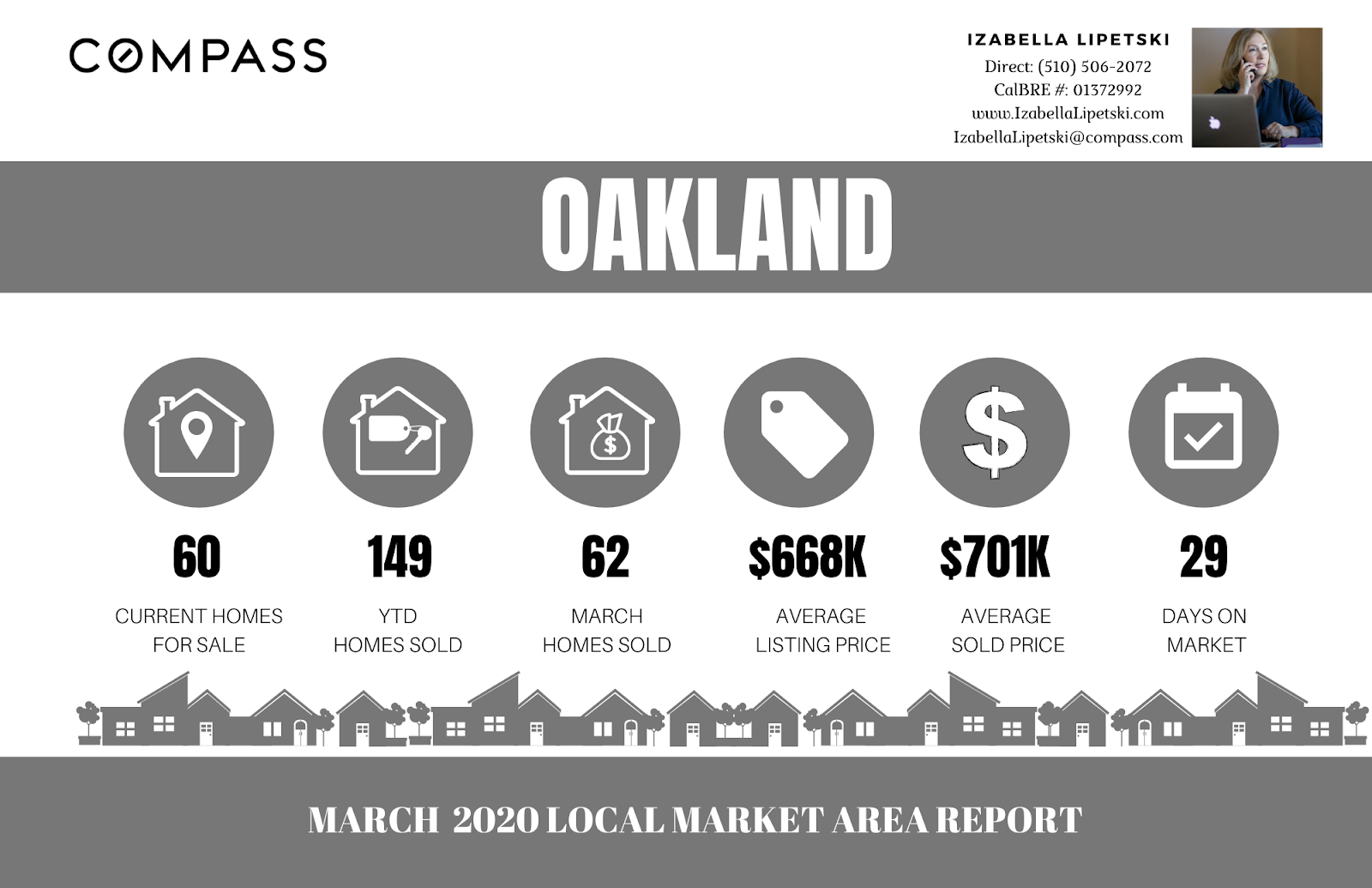

🏡 Buying or Selling Your Home? It's always a good idea to know what's going on in the market. 📊📈📉

Here's how the Real Estate Market performed FOR MAY 2020 for Pleasanton, Danville, Alameda, Oakland and San Ramon.

SINGLE DETACHED HOMES

Looking for your new home?

Check my WEBSITE for the hottest new listings in East Bay.

Thinking of buying or selling this year? When visiting isn't enough and you decide to make our beautiful area home, let me help you! From Single Family Homes, Condominiums, Luxury Houses and more, I am positive I can find the right home for you. Call or just text me at 510-506-2072 and let's get started!